Resiliq Launches Quant Lab: Quantitative Intelligence Built for Private Markets

Published on: April 20, 2026

Today, we are making Quant Lab generally available to all Resiliq platform users. Quant Lab is a purpose-built quantitative modeling environment designed from the ground up for private markets – where data is sparse, financials are irregular, and traditional tools routinely fall short.

Why Quant Lab

Private markets professionals have long relied on spreadsheets, ad-hoc databases, generic financial software, or expensive in-house quant teams to run the kind of rigorous quantitative analysis their investment decisions require. These approaches are slow, error-prone, and difficult to scale across a portfolio of active deals.

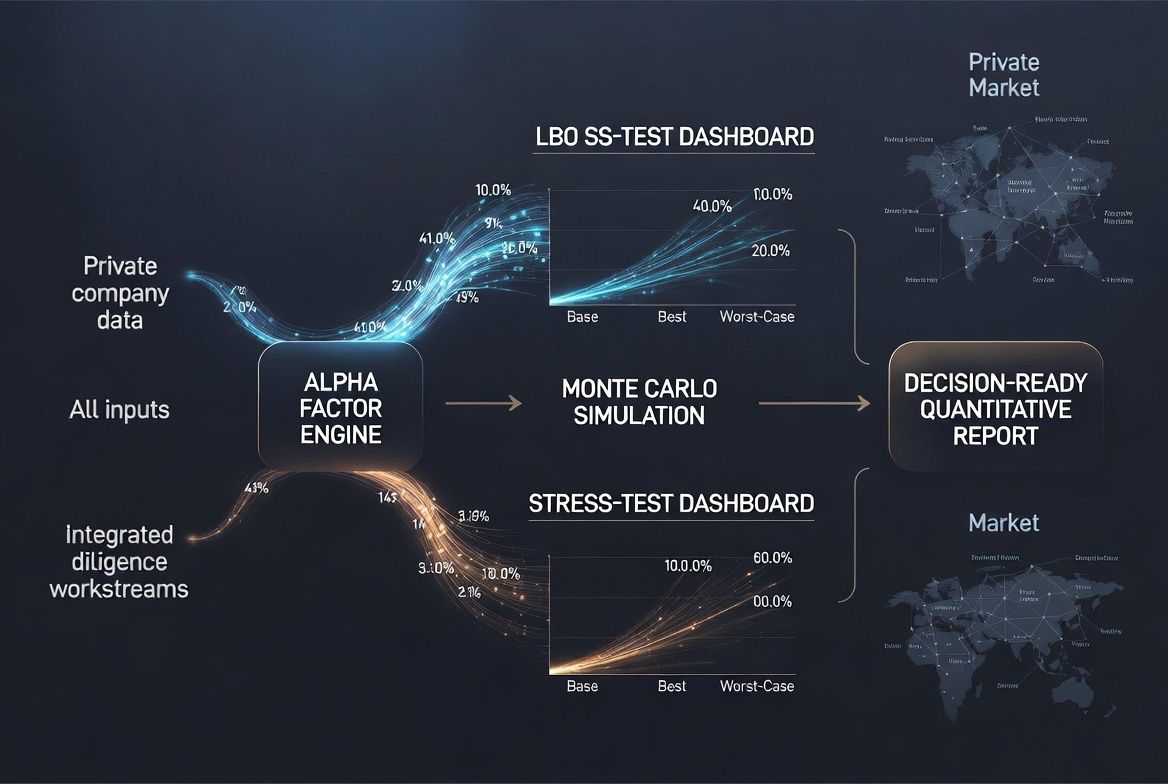

Quant Lab addresses this gap directly. It provides an integrated modeling environment within the Resiliq platform, offering pre-built quantitative models and scenario simulation capabilities that are specifically calibrated for the conditions of private markets – illiquid assets, limited comparable data, and non-standard financial reporting.

What Quant Lab Delivers

Pre-built models: A library of ready-to-use quantitative models covering LBO analysis, credit stress testing, LP/GP waterfall modeling, Monte Carlo deal simulation, and advanced AI/ML models. Each model is tuned to work reliably with the kind of incomplete and irregular data common in private markets.

Alpha factors: A curated set of alpha factors for screening and ranking investment opportunities across sectors, geographies, and deal types. These factors are a mix of private-market and common public market signals applicable to privates.

Scenario simulation: Run sensitivity analyses and stress tests across multiple deal parameters simultaneously. Understand how changes in entry multiples, leverage ratios, growth assumptions, or exit timing affect returns under realistic or not yet known private-market conditions.

Integrated workflow: Quant Lab is not a standalone tool. It is tightly integrated with the rest of the Resiliq platform – AI agents, deal & market research, due diligence, and portfolio monitoring – so quantitative insights flow directly into decision-making workflows.

Built for the Real Conditions of Private Markets

Most quantitative tools available today were designed for public markets, where data is abundant, standardized, and continuously updated. Private markets operate under fundamentally different conditions: limited historical data, non-uniform reporting, and long holding periods with infrequent pricing events.

Quant Lab is built to handle these realities. Its models are calibrated for sparse-data environments, its simulation engine accounts for illiquidity and irregular cash flows, and its output formats are designed for the reporting needs of PE, VC, and alternative asset professionals.

What This Means for Deal Teams

With Quant Lab, deal teams no longer need to choose between speed and rigor. An analyst can run a full LBO sensitivity analysis on a target company, stress-test the capital structure under multiple scenarios, and generate a decision-ready output – all within the same platform they use for sourcing, diligence and portfolio work.

This eliminates the friction of switching between tools, reduces the risk of model errors from manual data transfers, and ensures that quantitative analysis is grounded in the same data that drives the rest of the deal workflow.

Availability

Quant Lab is available now to all Resiliq platform users. Existing users can access it directly from their workspace. New teams can request access through support.

We will continue to expand the model library and simulation capabilities based on feedback from our users and the evolving needs of private markets professionals.

Related Solutions

Hedge Funds

300+ alpha factors and quant research agents built for private market data. Factor backtesting, ML model training, and derivatives analytics in one platform.

Private Equity

AI deal sourcing, LBO modeling, and AI due diligence for private equity. 20+ autonomous agents across financial, commercial, and tech workstreams.

Venture Capital

AI-powered VC workflow tools for thesis-driven sourcing, fast due diligence, and predictive portfolio monitoring. Find emerging winners before competitors.

Family Offices

Institutional-grade AI for lean investment teams. LP/GP waterfall modeling, multi-asset portfolio analytics, deal sourcing, and due diligence in one platform.

Related Articles

Deal-Making Revolution: How AI is Reshaping PE & VC

Discover how artificial intelligence is transforming PE and VC deal cycles – from AI-powered sourcing to automated due diligence and portfolio management.

November 15, 2024

Can Data Answer the α-Question in VC?

Explore how data-driven approaches in venture capital are evolving beyond simple data collection to AI-powered insights and systematic decision-making.

January 26, 2024